State of the Economy and Details on the CARES Act

Some market strategists are calling the end of the bear market already … do you think they’re right?

(Keep reading to see what could be behind the surge, as well as a breakdown of how the $2 trillion CARES Act affects your wallet.)

But first of all, I hope that anyone reading this is safe and well. If you landed on this page, we are connected in some way.

My family and I are doing well. I am in the office every day, while Sarah is working from home now that travel isn't possible for her at work. We've been reading together, - Stephen King's On Writing and Russell Brand's Recovery for me - working out and taking evening walks at home. With the world gone mad and shutting down, our home lives have become slower. We've enjoyed that.

I worry for those at hourly or at-risk jobs and for those that haven't saved. We are seeing a record number of unemployment applications and I know that means that many of us, our friends, and families will be hurting. The human cost of the virus and the economic fallout is not yet known. All we can do, if we're able, is put ourselves in a position to help those around us, and then help. However you can. Buy local, eat local, bank local, and invest local. Be considerate. Drive a little slower. Send a message to your neighbors that you haven't talked to in years and ask if they need help or supplies. We may get through this in weeks or this could be the new normal for a while - our economy will find a way to thrive and return to growth, it always has - it is all of us that will determine whether this makes us better or worse.

I have been encouraged by our government prioritizing individuals and small businesses, more than ever before, with the recent stimulus. And some of the largest corporations in the world are, right alongside all of us, shutting down and doing everything they can to fight this virus. We are, truly and globally, all together in this one. I find that encouraging.

Writing on the state of the market, recently, feels tasteless, so that’s why these blog posts have slowed down. But, these are also the times when financial planning and investment advice pay off the most. I know that emergency funds are boring and don’t get likes or clicks - but we are seeing RIGHT NOW why they are so important. And this applies to the entire financial plan. Financial advice is needed now more than ever; I know that, and it’s why I am still in the office every day. So, I’ll get out of my own head, and write on the state of this economy because we all need to know what is going on and what to do about it.

With markets whipping between rallies and retreats, it’s natural to ask:

Is it time to buy?

Is it time to sell?

Are we near the bottom?

Is the bear market finally over?

Despite the recent market surge, which propelled the Dow 21% higher in just 3 days (technically ending its bear market correction), it’s likely too soon to get overly optimistic.1

What gives? How can markets be rallying when the crisis hasn’t even peaked yet? When markets have fallen so much and “priced in” so much bad news, it’s common to see short-term surges on good news like the relief bill. However, these “head-fake” rallies can be unsustainable when there’s so much uncertainty.

Bottom line: No one is good enough to call the exact bottom of a market. What’s important is looking through the bear market to the other side and picking up opportunities along the way.

Whether the bear market is over or not, we’ve been here before and know what to do.

How worried should I be about a recession?

Cautious, but not panicked. When a $21 trillion economy comes to a screeching halt, there’s going to be an economic contraction. Multiple timely indicators show that we are already experiencing a sharp downturn.2

However, the $2 trillion fiscal rescue act and the Federal Reserve’s new asset-buying program are a double-barreled bazooka aimed at the effects of a serious recession.

We’re monitoring the data rolling in and will know more about how the economy is reacting to the unprecedented aid in the coming weeks and months.

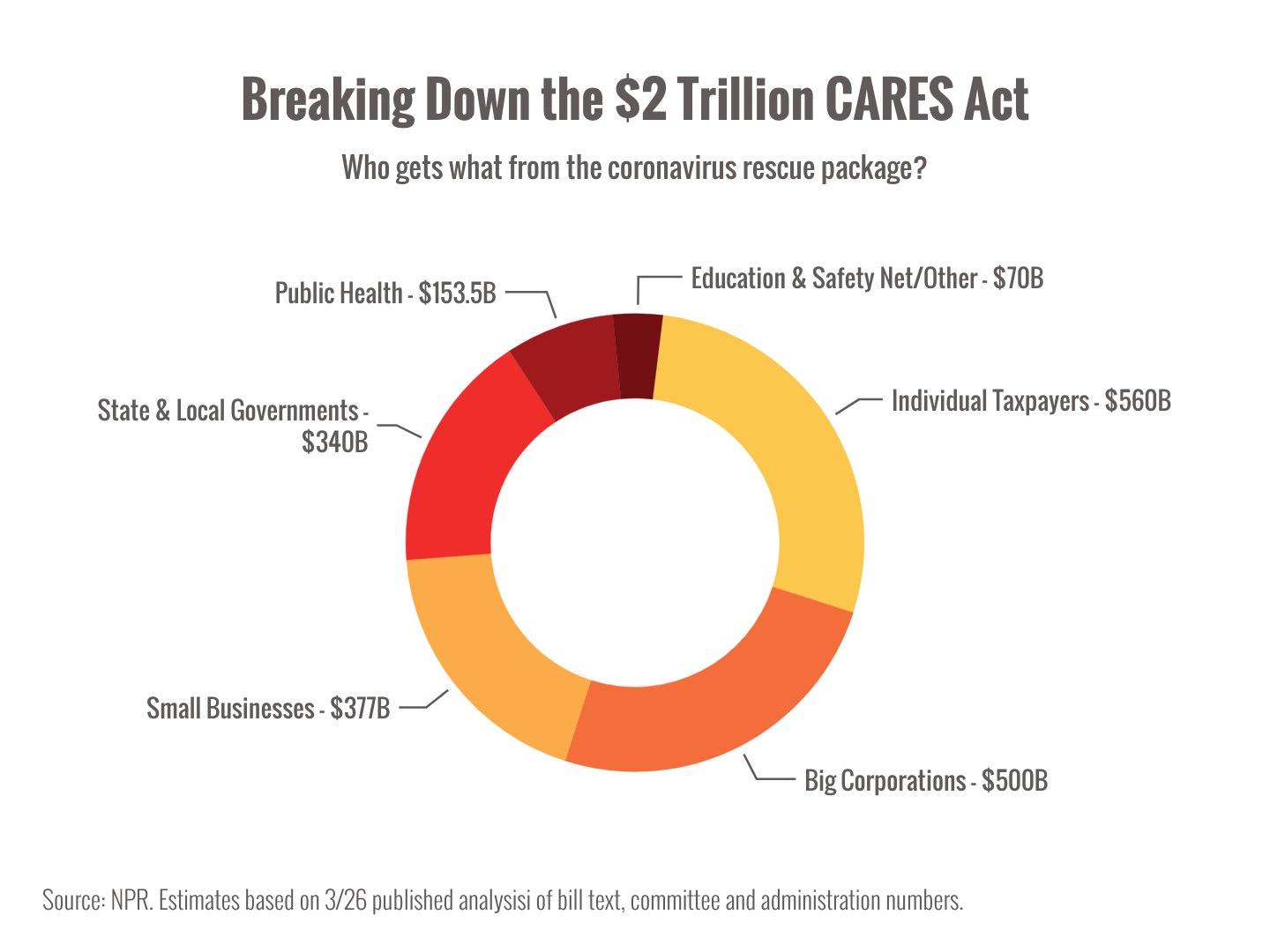

What’s inside the $2 trillion CARES Act? What’s in it for me?

The Coronavirus Aid, Relief, and Economic Security (CARES) Act is designed to provide relief for individuals and businesses who have been hurt by the outbreak. I won’t try to include all 800+ pages in this post, but here are a few key provisions that you should know about:3

One-time cash payment. Taxpayers are eligible for a one-time direct deposit of up to $1,200 per adult ($2,400 per couple) plus $500 per child under age 16. Amounts are reduced for those who make more than $75,000 ($150,000 if married). If you have filed your 2019 taxes already, the IRS will use that income to calculate your payment; if not, they’ll use your 2018 tax filing.

Better unemployment benefits. The Act will extend and expand unemployment insurance through Dec. 31. Eligible workers (now including self-employed, independent contractors, and gig economy workers) will receive an extra $600/week for four months, on top of what they receive from state unemployment benefits.

Early withdrawal penalty waiver. The Act waives the standard 10% early withdrawal penalty for eligible coronavirus-related distributions from retirement accounts (retroactive to Jan. 1). You’ll still pay income taxes on withdrawals, but you can spread them over a three-year period or use that time to roll the distribution back over.

2020 RMDs suspended. You won’t have to take a Required Minimum Distribution from your IRA or 401(k) this year, leaving you in control of how much you withdraw. If you already took your RMD for 2020, you have several choices: keep it and pay taxes on it, return it to your IRA as an indirect rollover, or convert the amount into a Roth IRA (Roth conversions are permanent).

“Client” means someone who is under my protection, and that extends to your loved ones.

Financial advice is a public service in these times, and I’m here to help. Please forward or share this post to any friends and loved ones who have been affected by the coronavirus and who might need some help. If you have questions about how the slew of recent changes could affect you, please call the office at (559) 740-0548 and we’ll find a time to talk.

- Schad TenBroeck, Sequoia Financial LLC

P.S. We’ve seen a rise in coronavirus-related phishing and identity theft scams. Please be on alert for “official-looking” emails asking you to open an attachment or click a link to read an official statement—they may contain malware. If you get a suspicious email, check the sender’s name and email address to make sure they’re not fake. When in doubt, just delete the email. Have someone in your life who you think might be at greater risk of email scams? Forward this to them so they're aware.

2https://finance.yahoo.com/news/ihs-markit-march-2020-flash-us-purchasing-managers-index-134651548.html

https://www.cnn.com/2020/03/26/economy/unemployment-benefits-coronavirus/index.html

3https://www.fidelity.com/learning-center/personal-finance/coronavirus-stimulus-package

https://www.washingtonpost.com/business/2020/03/30/coronavirus-stimulus-cares-act/

https://www.cnbc.com/2020/03/26/coronavirus-relief-act-expanded-unemployment-payment-and-eligibility.html

Chart source: https://www.npr.org/2020/03/26/821457551/whats-inside-the-senate-s-2-trillion-coronavirus-aid-package

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Schad TenBroeck is an Investment Advisor Representative of Sequoia Financial, LLC. Investment Advisory Services are offered through Sequoia Financial, LLC, a California Registered Investment Advisor. Insurance services are offered through TenBroeck Insurance Services. Sequoia Financial, LLC and TenBroeck Insurance Services are affiliated.